World-Class City. World Class Rent

Toronto has long aspired to be recognized as a world-class city, one that ranks among the top global hubs for finance, technology, medicine, and culture. Former mayor John Tory, as did his predecessors, described Toronto as “the best city in the world” and supported efforts to elevate its status alongside cities like London, New York, and Tokyo. But striving to be world-class comes with world-class costs. As housing prices and rents rise, it’s critical that affordability debates situate Toronto within its global peer group, not just in comparison to other Canadian cities.

In Canada, homeownership has traditionally symbolized success and security. Renting, by contrast, is often seen as temporary or second-best, something to be outgrown on the path to ownership. Popular discourse reinforces this view, with phrases like “paying someone else’s mortgage” casting renters as financially immature. Yet this narrative ignores how Toronto’s housing market has transformed over the past two decades, prioritizing real estate as an investment vehicle over livability and long-term community stability. As detailed in Part I of ‘Toronto at Home’, this shift has driven up home prices beyond the reach of many residents and increased reliance on the rental market.

Still, renting remains oddly absent from many affordability discussions or is treated as interchangeable with home prices. Headlines frequently conflate the two, e.g., ‘Toronto’s High Rent and Housing Costs Have Created a Crisis’ (Canadian Centre for Policy Alternatives, 2023) without differentiating the dynamics unique to renters. Yet, among 16 global cities analyzed, Toronto ranks 12th in terms of the share of households that rent, with 48.1% of households renting, well below global renter-majority cities like Berlin (84%), Vienna (82%), New York City (70.2%), and Paris (65.3%), but slightly higher than Stockholm (43%) and far above Singapore (9.2%). This reflects Toronto’s cultural emphasis on homeownership, even as the economic reality of buying has become unattainable for many. Yet when examining rental affordability, Toronto performs better: the average renter household spends about 30.9% of income on rent, which ranks 5th lowest among the 16 peer cities. Average renters in New York, Boston, and Vancouver pay significantly more relative to their income, often upwards of 60–100%. This contrast challenges the dominant narrative that Toronto is among the most unaffordable cities for renters. In fact, Toronto’s rent burden is more moderate compared to many of its global peers, suggesting that while housing pressures are real, rental affordability in relative terms may be more manageable than often portrayed. Still, with nearly half the city renting, ensuring an adequate supply of diverse, high-quality rental housing remains critical to supporting Toronto’s workforce and maintaining economic competitiveness.

Toronto Rental Market Affordability. Will it Last?

Toronto’s housing market has notably cooled since 2022 highs. Sales volumes in early 2025 are well below last years levels and inventory is at multi-decade highs (buyers’ market conditions). For example, April 2025 GTA home sales (5,601 transactions) were about 21% lower year-over-year, even as active listings hit a record 27,386. However, prices have only edged down a few percent in response. In Toronto proper, the median house price was $950,000, down 3.2% from the previous year. Overall, these indicators suggest modest price declines and abundant supply as of spring 2025. In tandem, the rental market has also softened as supply has risen. Vacancy rates have climbed (Toronto’s vacancy was about 3.7% in Q1 2025) while rents only recently started to decline.

Between 2022 and 2024, Toronto experienced a significant increase in purpose-built rental (PBR) housing completions. Notably, in the first quarter of 2025, 2,136 PBR units were completed, marking a 173% increase compared to the same period in 2024 and representing the second-highest quarterly total in the past 30 years. This surge in completions contributed to a 2.5% expansion of the rental stock within the City of Toronto in 2024. This is good news for renters. However, despite this uptick in completions, the initiation of new PBR projects have come to a standstill. To date in 2025, only 731 PBR units commenced construction in the Greater Toronto and Hamilton Area (GTHA), a 60% drop from the same period in the previous year and 41% below the five-year average. This slowdown is attributed to factors such as high financing costs, declining rents, and increased competition from condominium rentals, which have made new PBR developments less financially viable. Indeed, some of the easing of rental costs have been driven by the growth of active condo rental listings, which are up 29% above last year’s level, and average condo rents fell 2.8% year-over-year in Q1 2025 (urbanation.ca). However, these condo rental units are not guaranteed to stay on the market. By policy the City of Toronto does not treat condo units as permanent rental housing and analysts warn that investor-owned condos are likely to subsequently revert to owner occupied use (chra-achru.ca). So, although investor-owned condo rentals have eased pressure in the short term, they can be withdrawn or sold at any time, unlike purpose-built rental (PBR) apartments, making the long-term rental supply inherently more fragile.

In short, while there has been a slight reprieve in rental costs due to supply – this trend might be short lived. With few PBR’s being constructed, and the possibility of condo’s reverting to owner occupied use, we may well see rental shortages and increasing rents during the next economic upturn.

Unintentional Retrenchment of Perceptions

City of Toronto and Federal policy documents often conflate rental housing with affordability and homelessness. The HousingTO 2020–2030 plan, for example, sets a target of 40,000 new affordable rental units (20% of which must be deeply “rent-geared-to-income” or supportive for homeless people) by 2030. In Council reports on new rental incentives, staff explicitly emphasize providing “homes affordable for residents in greatest need, including rent-geared-to-income and supportive homes for people experiencing homelessness.” Similarly, the City’s equity statements for rental programs stress serving “vulnerable and marginalized” groups via new affordable rentals. This emphasis on affordability and social housing within rental policy signals to the public that rental supply is primarily an issue of low-income housing. In practice, the word “rental” in City planning is often framed as part of solving homelessness or affordability crises. As one City of Toronto document, Perspective on the Rental Housing Roundtable notes, Toronto’s rental targets focus on “affordable rental” and “supportive housing” metrics rather than standard market rentals. The paper indicates that Toronto, in fact, is facing two housing crises – one in which rising rents have made it increasingly unaffordable for middle income earners to live in the city; and a second crisis of affordable and supportive housing for the homeless or who are experiencing family, physical, mental health and addiction struggles. The paper argues that these intersecting, but separate crises require different policy solutions, but too often in Toronto, they are treated as the same issue.

Renting Normalization in Other Cities

In most other global peer cities, long-term renting is far more normalized across all age and income groups. With home prices so steep, even middle-class professionals often rent for decades. There is less stigma because renting is simply the majority experience. In NYC a clear majority rent their homes, including many affluent households. London similarly has a huge rental sector (especially private rentals and also council housing), making renting a common and accepted living arrangement for life. Vienna and Berlin takes this even further, with most residents renting, and there is traditionally no assumption that one must buy a home. Renting is a standard, socially accepted tenure even for families and higher-income earners. Culturally, Germans have not treated homeownership as a status symbol in the way North Americans or the British often do, and strong tenant rights make lifetime renting secure.

Class and Status Views

The result of these norms is that Toronto’s renters may face more of a class/status perception gap than renters in NYC, Paris, London, or Berlin. In Toronto, a common attitude has been that renting is what you do in your 20s or when you “can’t afford a house yet,” implying that success means eventually buying a property. Homeownership is seen as a milestone of adulthood and a source of pride for many Canadians. By contrast, in cities like New York, there isn’t the same presumption that a successful 40-year-old must own a home; plenty of well-to-do New Yorkers rent by choice or necessity, and it’s not automatically viewed as a lower status. Berlin’s renters span all classes, so there is little social stigma attached to not owning – it’s entirely normal for even high-earning professionals or seniors to rent their whole lives. That said, as housing affordability challenges persist in the GTA, Canadians are slowly questioning the old narrative – The Walrus (2025) recently asked, “Many Canadians will never own a home. Does it matter?”, noting that renting is becoming a permanent reality for more people in Toronto and Vancouver. In summary, Toronto’s culture is still catching up to the idea of renting as a respectable, and long-term choice. Yet, the public narrative often lags behind these nuances: it paints a picture of an impossible rental market, without acknowledging that Montreal remains a much less expensive alternative within Canada, or that Toronto is not the worst-case scenario globally. Nevertheless, Toronto’s renters do spend a very large share of income on housing on average, and many are justifiably anxious about affordability and stability.

Crucially, beyond the numbers lies the cultural narrative. In Toronto, renting has historically been viewed as a stepping stone, overshadowed by a strong pro-ownership ideology. This contrasts with cities where renting is a normalized, even predominant way of life. Such perceptions influence policy and personal decisions: a society that valorizes ownership may invest less in tenant protections or rental supply. Combined with a market that treats housing as an investment commodity, the result in Toronto has been high costs and a sense of rental precarity. Shifting this dynamic – by learning from cities where renting is ordinary and by rebalancing housing toward its purpose as a home – will be key to improving long-term affordability and the renter experience. In sum, while Toronto’s renting situation is not uniquely dire when weighed against other cities, addressing the affordability challenge will require both continued supply growth and a cultural-policy pivot away from viewing housing chiefly as an investment or as the primary solution to homelessness.

Affordability is Important to a High Functioning Labour Market

Affordable rental housing is a foundation for robust labour supply. Studies show that without ample rental options, workers are forced to migrate to cheaper areas or become cost burdened. In turn, employers cannot draw on a full talent pool. For example, if nurses, teachers or tradespeople can’t afford to live in Toronto, companies and institutions lose skilled staff or even relocate. Economic analyses confirm that ample housing supply is linked to productivity and growth, places with severe shortages “limit labour mobility” and struggle to attract firms. In practice, affordable rentals enable broader labour participation: younger and lower-income workers (who are more likely to rent) can take jobs in the city without untenable housing costs.

Moving Forward

Rather than viewing renters as primarily a temporary or lower-income group, Toronto must fundamentally rethink how it values rental housing and the people who rely on it. Nearly half of Toronto’s households are renters representing a cross-section of workers, families, seniors, and newcomers who keep the city running. In global cities like Berlin, Vienna, New York, and London, renting is normalized across all income levels and life stages; it is not seen as a failure to own, but as a legitimate and often preferred long-term option. Toronto, by contrast, still carries a cultural narrative that equates renting with transience or financial inadequacy, a view that no longer aligns with the city’s economic or demographic realities. As housing prices have surged out of reach for much of the population, renting has become not just a stepping stone, but a permanent and necessary part of urban life.

But Toronto’s rental market cannot meet this challenge without serious and sustained policy support. Over the past 24 months, the number of construction jobs in Toronto has declined by more than 8%, and the number of job postings in the housing construction sector has plummeted by 80%, a clear warning sign that private-sector investment is stalling. Developers are pulling back from purpose-built rental projects due to rising uncertainty, costs, regulatory complexity, and competition from condominium units. If the city wants to ensure stable long-term rental supply, it must act decisively: expedite approvals, reduce fees for purpose-built rentals, offer property tax relief, and treat rental housing as a priority class of development. The City of Toronto has taken a few steps towards this. Let’s continue to unleash the market, not through deregulation, but through smart policy that de-risks rental construction and enables it to scale. Toronto cannot afford to wait. The foundation of its economy, young construction workers who were promised bright futures and high earnings, and livability depends on getting this right.

When a Place to Live Became an Investment

In the 1960s, a Portuguese family who had recently arrived in Toronto settled in Hillcrest Village, a quiet neighborhood just west of the city’s bustling downtown. The father, working a steady job in one of the city’s many manufacturing plants, and the mother, perhaps sewing in a factory or cleaning houses, could afford to buy a modest home on their combined wages. Back then, a house was simply a place to live, a refuge for raising children and building a life in a new country. For newcomers like them, homeownership wasn’t about wealth-building or speculation—it was about stability, community, and opportunity. Fast forward to today, and for that family, new to Canada and starting their first jobs, buying a home feels like a distant dream. The city’s housing market has transformed into one of the most expensive in the world, driven by decades of financialization, speculation, and skyrocketing demand. This shift hasn’t just left aspiring homeowners behind; it’s also rippled through the rental market, creating deep inequalities in housing access and affordability.

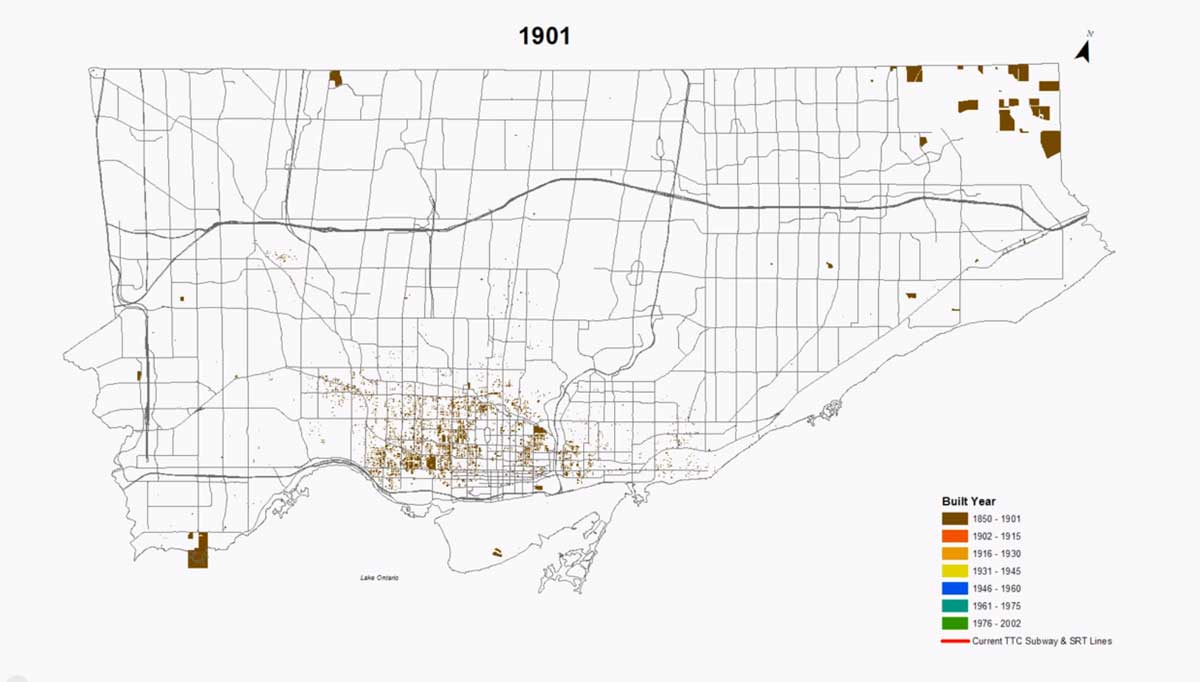

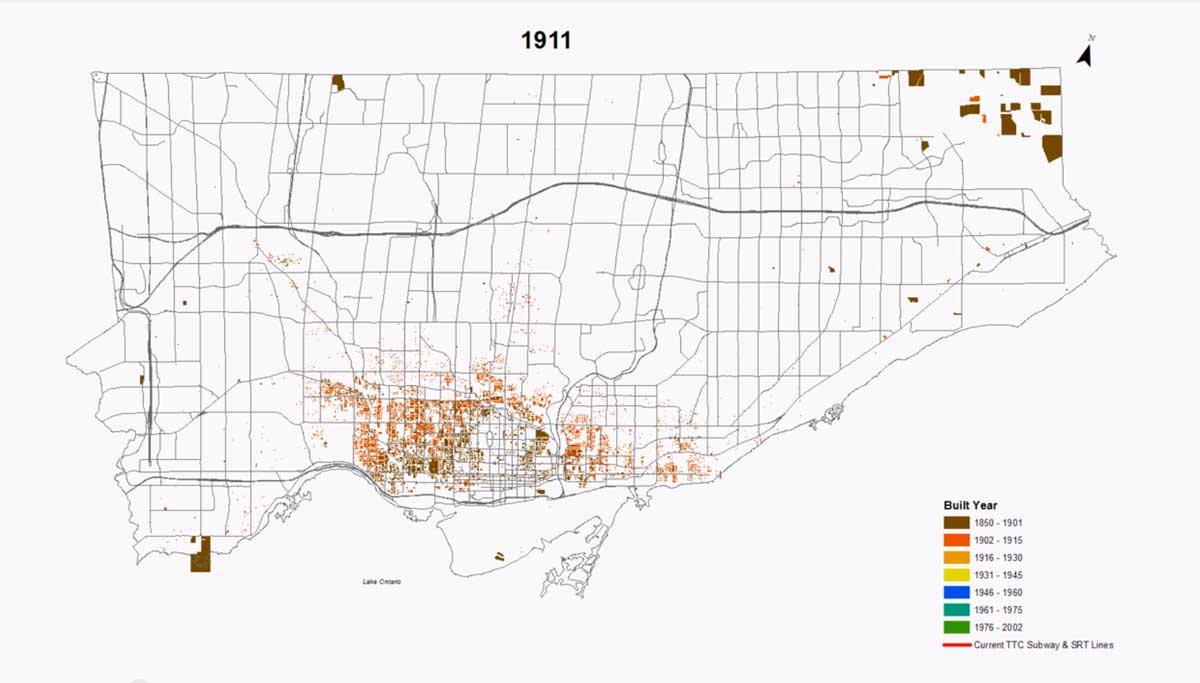

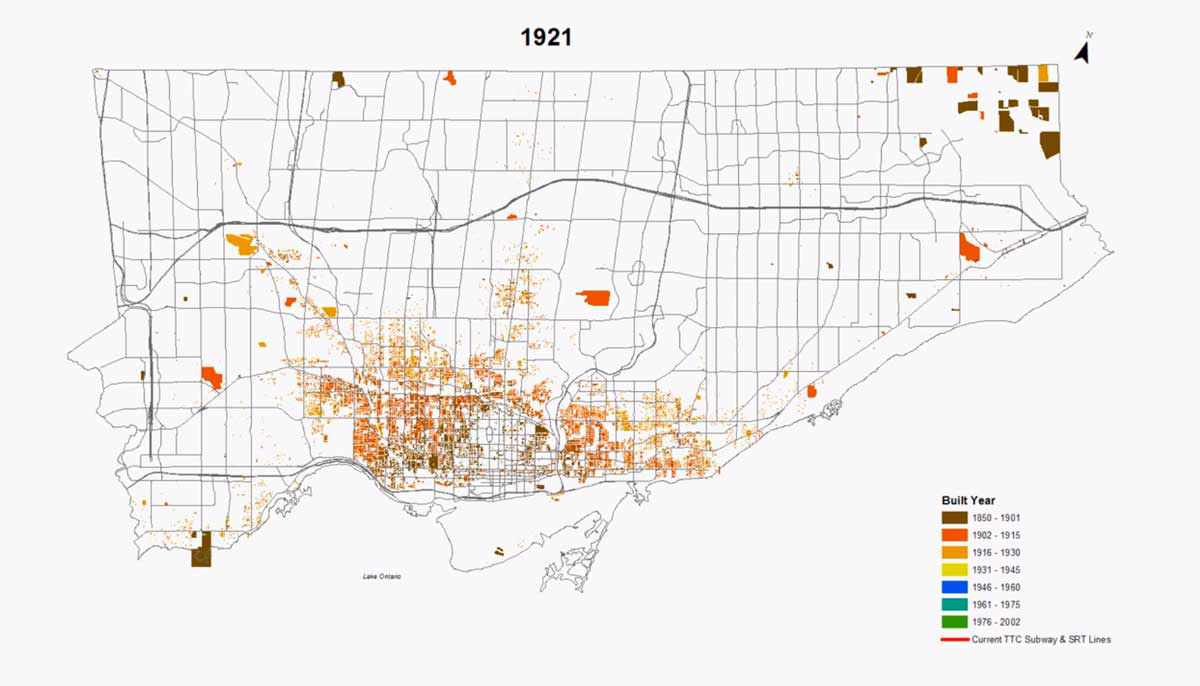

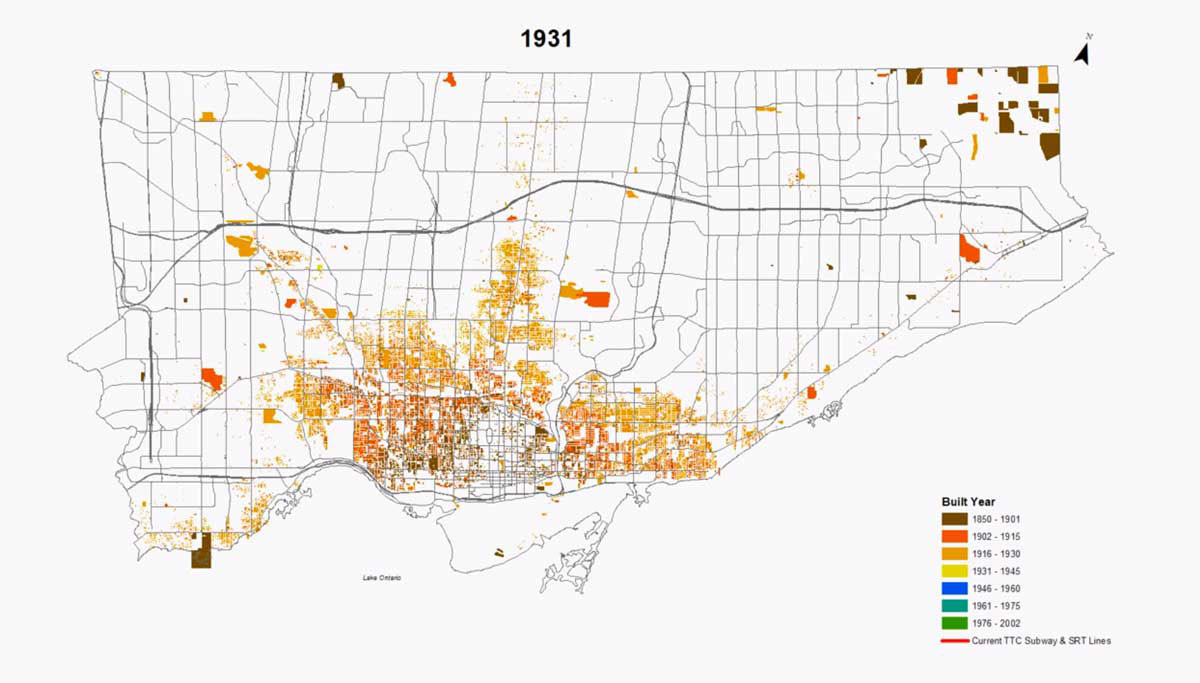

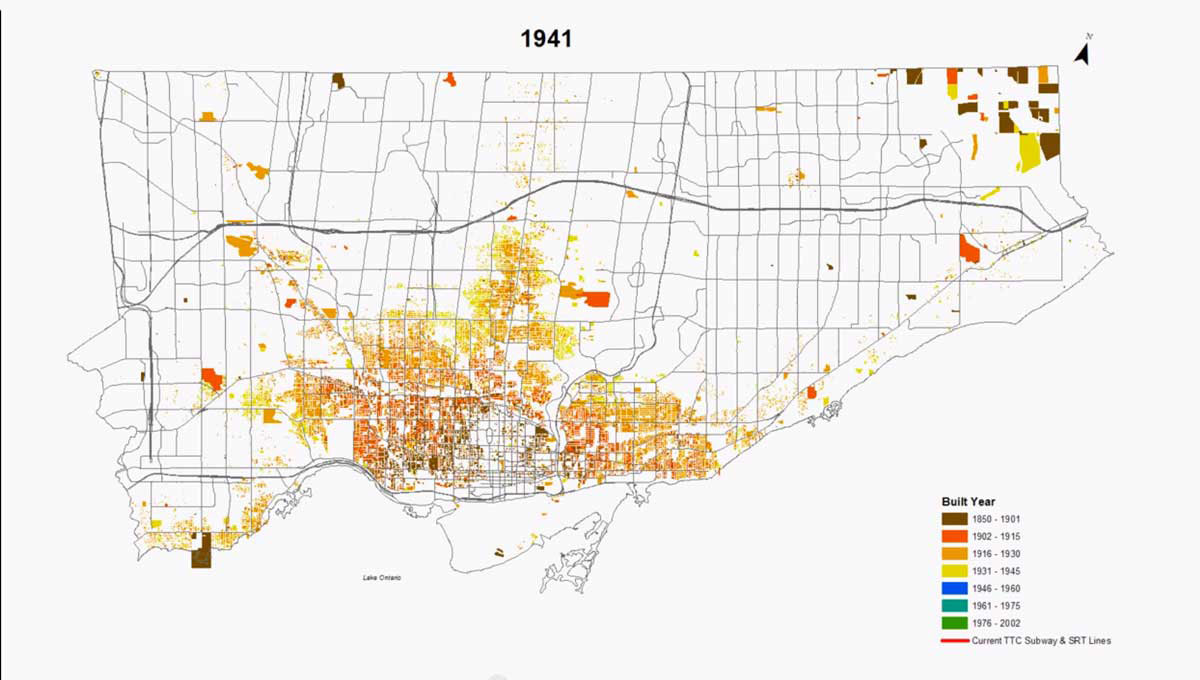

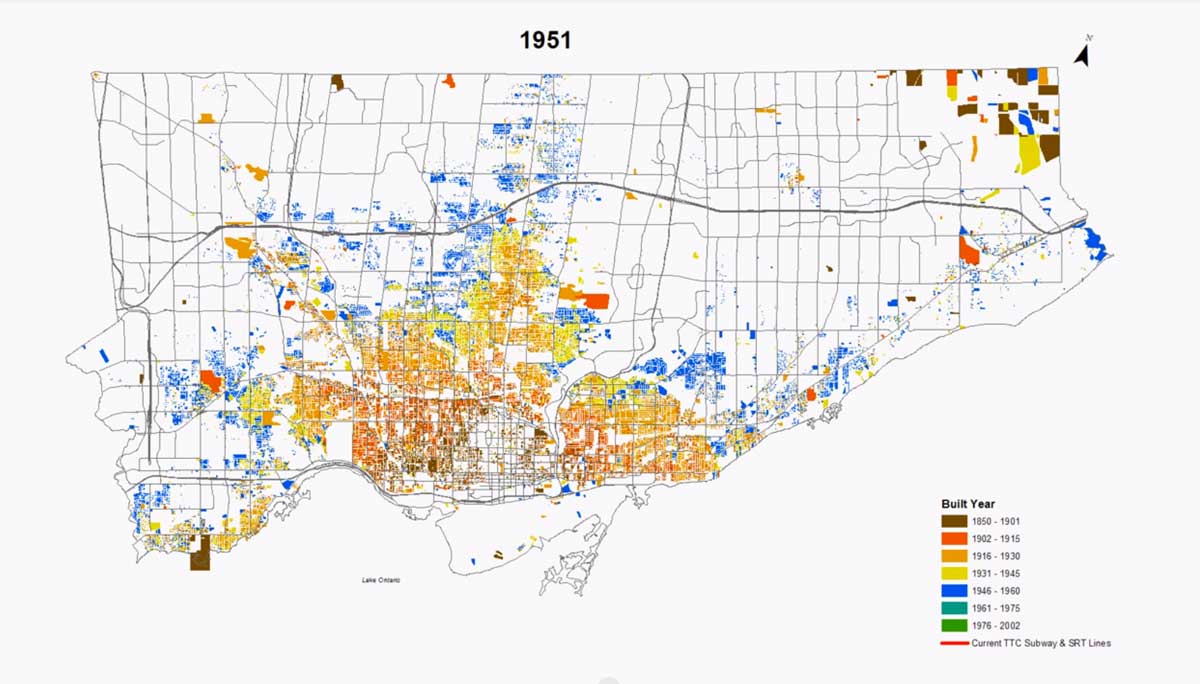

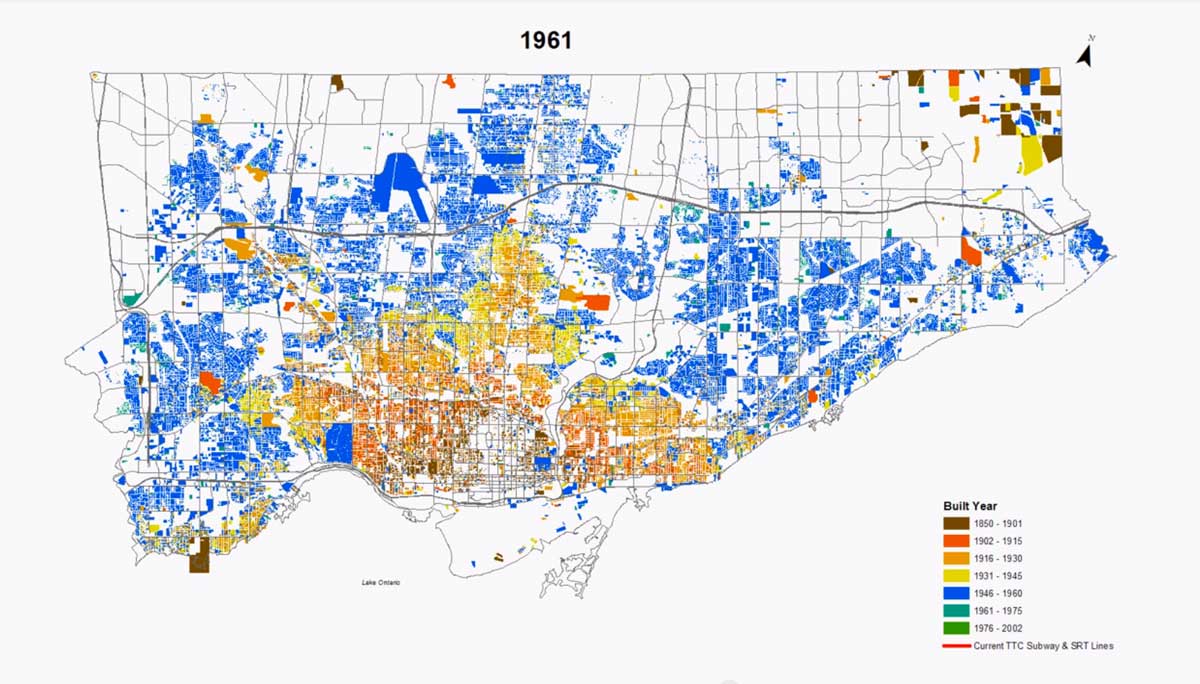

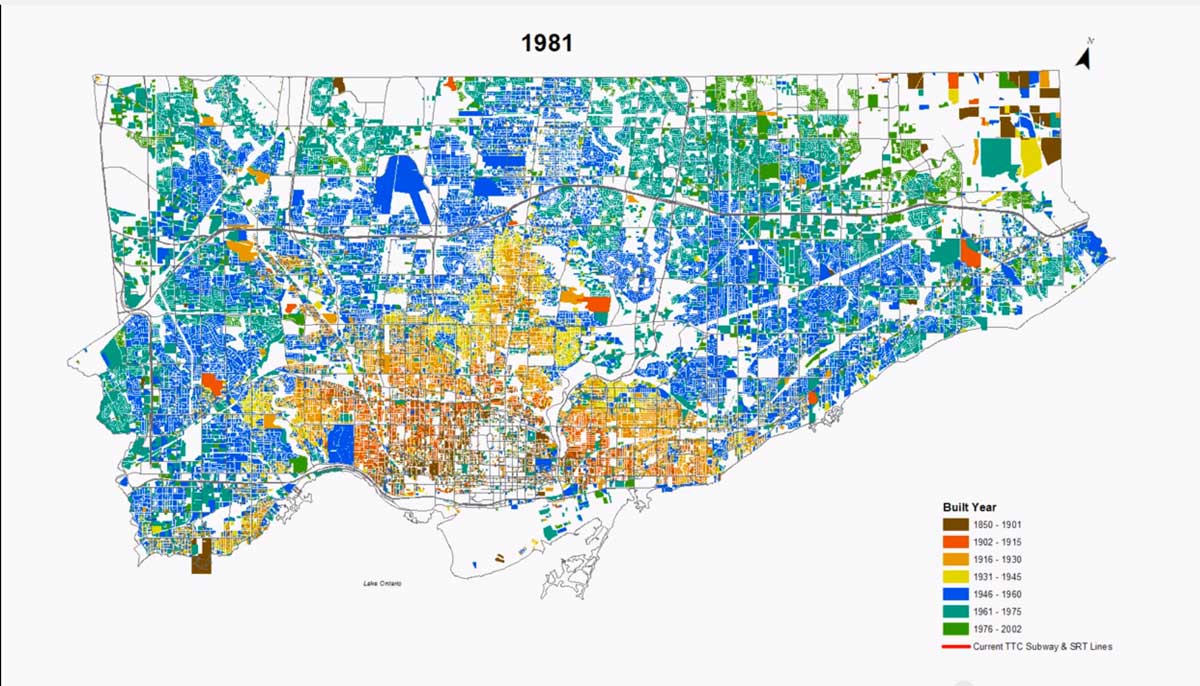

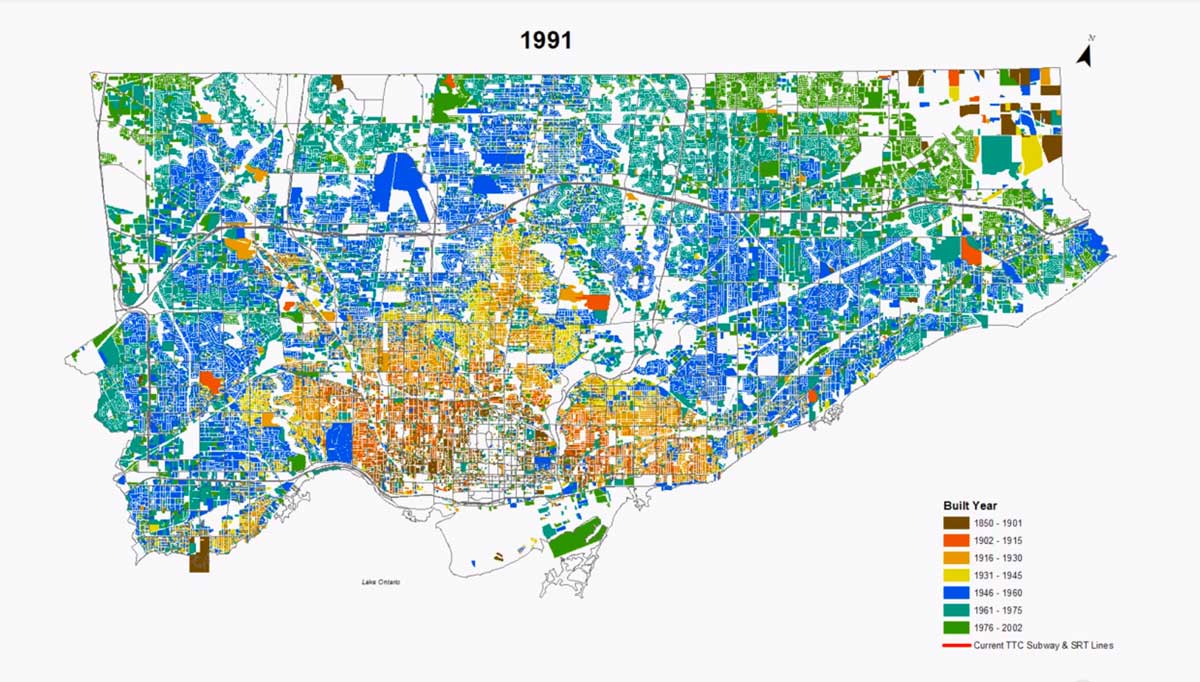

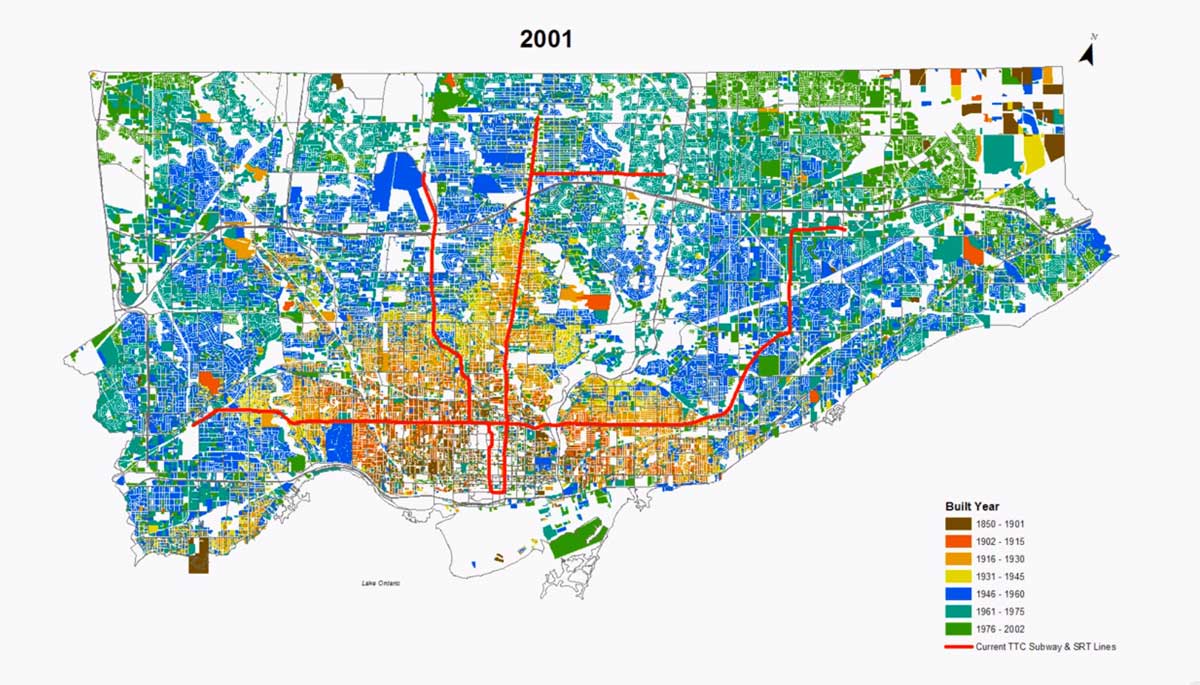

In the decades following World War II, Canadian housing policy reflected a national commitment to stability and prosperity. Homeownership was promoted as a cornerstone of community building and economic recovery, supported by initiatives like the National Housing Act of 1944. In cities like Toronto, working families—often recent immigrants—could afford modest homes in emerging suburban neighborhoods such as East York, West Hill, Bayview Village and Mimico, even on a single income. Housing prices remained stable, aligned with wage growth, and homes were primarily viewed as places to live, not as financial assets. The post-war housing boom, driven by accessible mortgages and affordable construction, allowed millions to achieve homeownership, forming the foundation of the Canadian middle class.

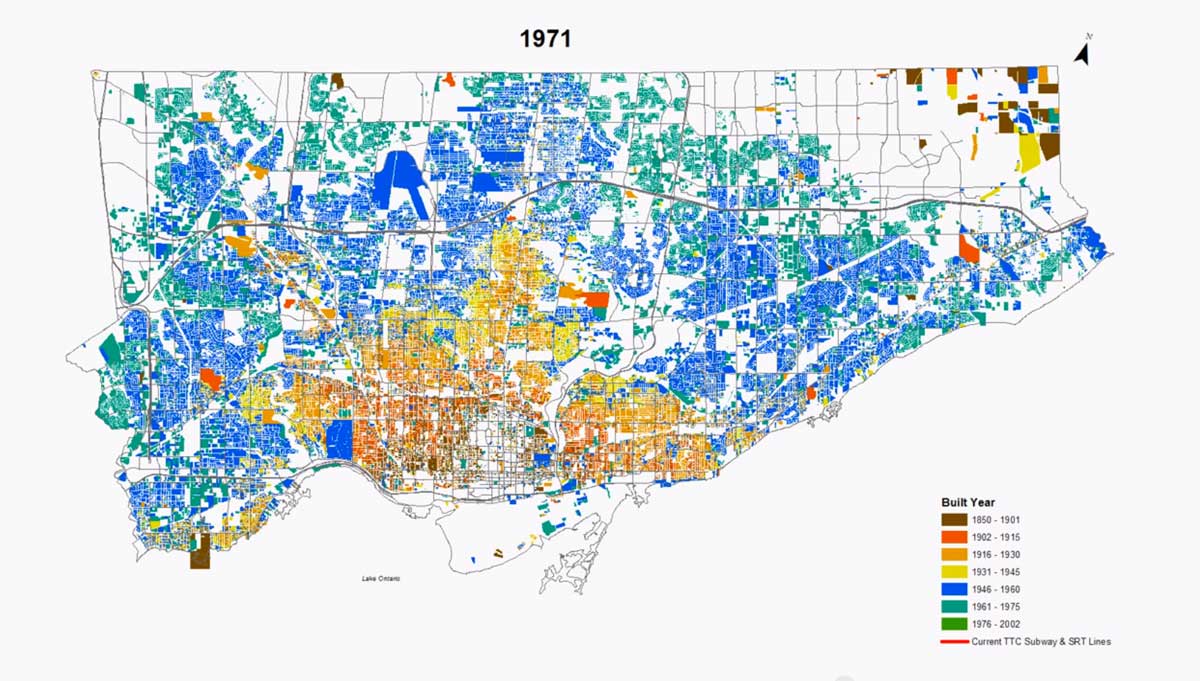

By the 1980s however, the dynamics of homeownership began to shift in response to broader economic and policy changes. Reforms led to financial deregulation, which expanded access to credit and facilitated higher levels of borrowing. The Canada Mortgage and Housing Corporation (CMHC) pivoted from its original focus on affordable housing to insuring mortgage debt, enabling riskier lending practices. Toronto, as a rapidly growing global city, became increasingly attractive to foreign investors seeking safe and appreciating assets. Housing was no longer seen merely as a dwelling but as an investment vehicle; a cultural shift reinforced by public policies like tax exemptions on primary residence capital gains. Real estate began to serve dual roles: a source of shelter and a key driver of wealth accumulation.

While housing prices increased during the period of 1965 to the early 2000’s (although it is worth noting that during the first part of the 1990’s, housing prices declined), it was not until 2005 that housing prices started to dramatically shift upwards. Historically low interest rates over a sustained period made investment in houses more attractive while returns on fixed-income investments like bonds and savings accounts were far less attractive. As seen in the graph below, Toronto housing has increasingly been perceived as a low-risk, high-return investment, outperforming traditionally safer assets like bonds while avoiding the volatility of stocks. While stocks have historically provided the highest returns, their short-term fluctuations and economic sensitivity make them riskier. Bonds, once considered the safest investment, have faced challenges from inflation and interest rate fluctuations, reducing their appeal. In contrast, housing in large metropolitan areas has been increasingly viewed as a stable wealth-building asset, particularly in cities like Toronto, where prices have rapidly risen.

The current home buyer (or investor) is unlikely to remember the 1990s real estate crash, or if they do, it is considered an anomaly. In short, buyers and investors increasingly perceived housing as a secure investment that offered both stability and superior long-term returns when compared to bonds or even stocks. A cursory review of housing advertisements spanning from the early 2000’s to current times demonstrates an increased focus on housing as an investment. The proliferation of marketing content and advertising strategies are aimed at real estate investors. From the early 2000’s on, residential ads began to commonly emphasize terms like “investment property,” “ROI,” and “rental yields,” underscoring the financial advantages of housing as an investment.

Toronto has one of the lowest property tax rates in North America while imposing some of the highest development charges for housing. This combination drives up home prices, creating an environment that benefits existing homeowners while making it harder for new buyers to enter the market. Toronto’s tax rates have been comparatively low for over 40 years, contributing to higher housing costs as local and foreign investors prefer cities with lower holding costs, fueling speculation and reducing the supply of homes for end-users, ultimately pushing prices higher.

Meanwhile, a study by Altus Group Economics found that Toronto’s development charges are among the highest in North America, particularly for low-rise housing. Government-imposed charges in Toronto are, on average, three times higher per unit than in most U.S. metropolitan areas and about 1.75 times higher than in other Canadian cities. These elevated development fees increase the overall cost of housing, as developers pass these costs on to consumers. In effect, the city’s policies—whether intentional or not—disproportionately favour existing homeowners by keeping their tax burdens low while shifting the cost of growth on to future residents.

The concept of housing as an investment, combined with historically low interest rates, Toronto’s population growth (one of the fastest growing cities in North America), and restrictive zoning policies created significant pressure on Toronto’s housing supply, fueling an unprecedented surge in home prices. Between 2000 and 2023, average home prices in the city increased by over 300%, fundamentally altering the accessibility of homeownership.

The redefinition of housing as an investment has had significant spillover effects on Toronto’s rental market. Skyrocketing home prices pushed more residents into the rental market, driving average rents for a one-bedroom apartment to over $2,500 per month by 2023. This convergence of factors created a cascading effect: tenants faced higher rents, displacement through “renovictions,” and increasing housing insecurity. Purpose-built rental developments, which once played a crucial role in providing stable, affordable housing, stagnated as developers focused on more lucrative condominium projects.

And why not? Ontario’s rent control measures, first introduced in 1975, were well intentioned and designed to protect tenants from rapid rent increases as inflation hovered above 10% and with a peak of 20% in 1981. The 1986 Residential Rent Regulation Act further tightened restrictions, limiting how much landlords could charge even for new tenants. By 1992, the provincial government introduced vacancy control, preventing landlords from adjusting rents to market levels after tenants moved out. While these policies provided stability for renters, they had an unintended consequence—discouraging the development of new purpose-built rental housing. With capped rent increases and restricted profitability, developers and investors shifted their focus away from long-term rental buildings in favor of more lucrative condo developments, significantly reducing the supply of new rental units.

As purpose-built rental construction declined, landlords and investors sought alternative ways to maximize returns. Many turned to short-term rentals, which were not subject to rent control regulations, leading to a surge in Airbnb and Vrbo listings. By 2019, over 20,000 housing units in Toronto were operating as short-term rentals, further tightening the already constrained rental market. While rent control has helped protect existing tenants, it has also made it much harder for newcomers to find housing. With limited rental supply and landlords preferring to keep long-term units off the market or convert them into short-term stays, new renters face fewer options, higher competition, and steep rental prices in unregulated units. The result is a housing system where long-term tenants benefit from stability, but newcomers struggle to secure a place to live, further deepening Toronto’s affordability crisis.

The consequences of housing as an investment first are profound. Wealth inequality has widened, with long-time homeowners and investors benefiting disproportionately from rising property values while younger generations and renters struggle to gain a foothold in the housing market. The city’s reliance on real estate growth and development fees as an economic driver has heightened vulnerability to market corrections, creating risks for broader economic stability. Socially, the housing crisis has deepened inequities, delayed life milestones such as starting families, and fragmented communities as long-term residents are displaced.

It is likely that only a catastrophic economic event will change the perception that housing is a low-risk and high reward investment. Yet such an event would send shockwaves through the economy, wiping out homeowner and generational wealth, triggering foreclosures, and leaving many in negative equity. Banks, heavily exposed to mortgages, could tighten lending, while job losses in construction and real estate would surge. Governments, reliant on property tax, development and land transfer revenues, might face spending cuts or tax hikes. While housing affordability would improve, the pain of the cure dramatically outweighs the benefit. With so much of Ontario’s economy, financial system, pension funds and personal wealth tied to housing, the market may be too big to fail, forcing policymakers to step in to prevent a full-blown collapse, even as they struggle to make housing more affordable.

Restoring housing as a foundation for community and not merely wealth accumulation—will require serious thought and policy interventions. In the next installment of Toronto at Home: Building on Shifting Ground, we will explore how Toronto’s housing market evolved from providing for both residents and newcomers to falling short of meeting the city’s growing needs, and how neighborhoods have shaped—and been shaped by—this shift.